Understanding Life Insurance: A Financial Safety Net or Just a Funerary Fund?

Understanding Life Insurance is crucial for making informed financial decisions. At its core, life insurance serves as a financial safety net for your loved ones in the event of your untimely passing. It provides a death benefit, which can cover daily expenses, outstanding debts, and ongoing financial obligations such as mortgage payments and children's education. However, many people misconstrue it as merely a funerary fund, thinking its only purpose is to cover burial costs. This limited view neglects the broader financial protection it offers, ensuring that your family can maintain their standard of living even in your absence.

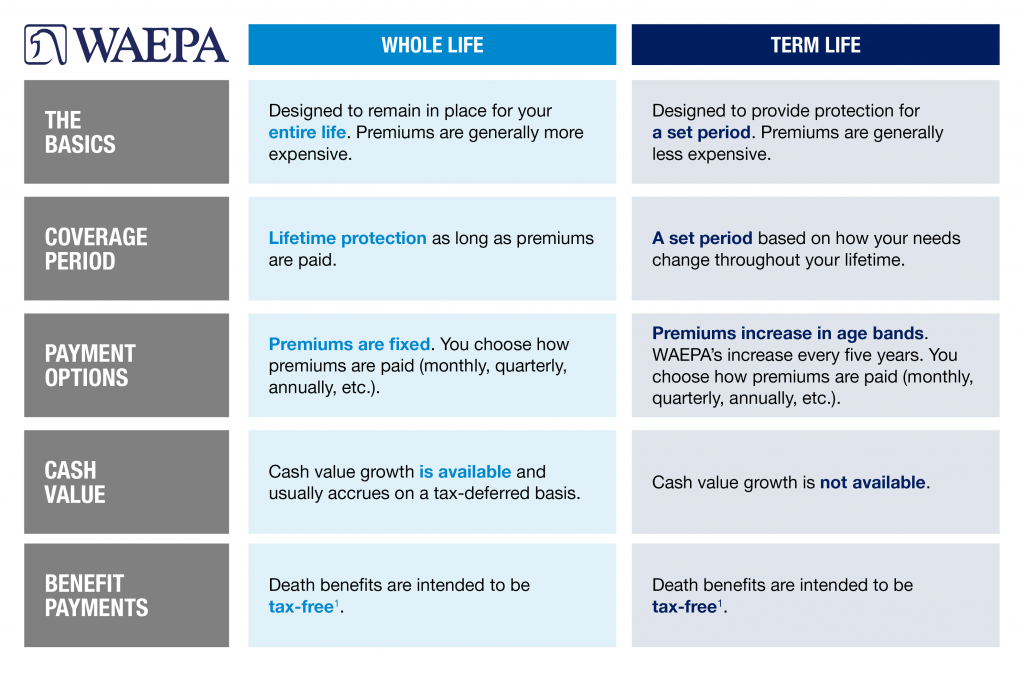

When evaluating life insurance, it's important to assess the different types available. Term life insurance provides coverage for a specified period, while whole life insurance offers lifelong protection and builds cash value over time. According to Forbes, understanding these options can help you determine what best suits your family's needs. Ultimately, life insurance is more than just a safety net; it is a proactive approach to financial planning that can safeguard your loved ones' future.

Is Life Insurance a Smart Investment or Just a Mourning Expense?

When considering whether life insurance is a smart investment or merely a mourning expense, it's crucial to evaluate its benefits beyond just funeral costs. While many people perceive life insurance as a way to cover immediate expenses after a loved one passes, it can also act as a financial safety net for dependents. According to the Investopedia, life insurance provides the necessary funds to replace lost income, pay off debt, and cover children's education, making it a valuable component of long-term financial planning.

However, some argue that life insurance can be seen as a mourning expense, designed to provide peace of mind rather than tangible returns. Critics suggest that the money spent on premiums could often yield better returns if invested elsewhere. The Forbes article highlights that while insurance is essential for risk management, individuals should balance it with other investment options to ensure a diversified financial portfolio. Ultimately, assessing personal financial goals will guide whether life insurance is a wise investment or just a necessary expense during times of grief.

What Happens to Your Life Insurance Benefit When You Pass Away?

When you pass away, your life insurance benefit is designed to provide financial support to your beneficiaries. The process begins with the designated beneficiaries filing a claim with your insurance company. This claim typically requires the submission of a death certificate and may include other documentation to verify the death and the beneficiaries’ identities. Once the claim is approved, the insurer will release the funds specified in your policy, ensuring that your loved ones have the financial resources to manage outstanding debts, funeral costs, and everyday living expenses. For more detailed insights into this process, you can visit NerdWallet.

It is important to understand that the life insurance benefit is generally paid out tax-free to your beneficiaries. However, issues may arise if the policy has not been kept updated, such as outdated beneficiary designations. In addition, if your policy carries a cash value component, your beneficiaries will receive the greater of the death benefit or the policy's cash value at the time of your passing. More information on what happens to life insurance proceeds can be found at Investopedia.